Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

-

Individuals

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

-

Employers

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

-

Institutions

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

-

Financial Professionals & Brokers

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

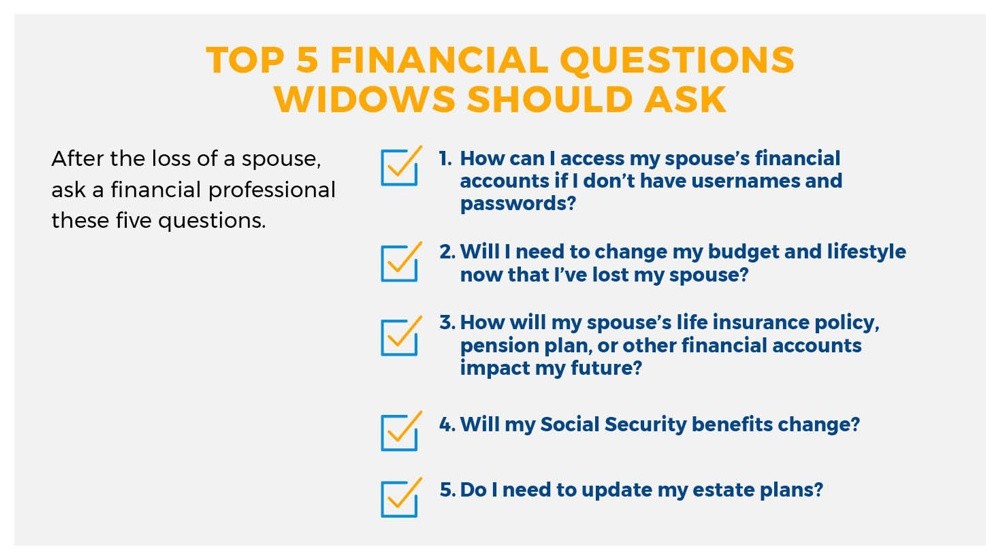

The loss of a significant other can offer an opportunity to learn about financial empowerment.

There are few events in life as devastating as losing the person who knows you best, and with whom you have spent years or even decades in a relationship. You may be more stressed than ever before—in your adult life, the death of a spouse ranks higher than all other stressors.1

As a widow, you are facing the most difficult emotional challenges in the days immediately after your loss. And if you’re older, you are more likely facing symptoms of depression as you grieve.2 And, on top of all the emotional and social issues you must face, there are also significant financial steps that should be taken as soon as possible, especially if you were not the financial decision-maker in your relationship. Luckily, there are reliable resources and professionals who can help you through this difficult time.

Become the Family CFO

By 2030, American women are expected to control much of the $30 trillion in financial assets that baby boomers will possess—a potential wealth transfer of such magnitude that it approaches the annual GDP of the United States.3 For widows who have not previously been in charge of financial decisions, your first step is to locate all of your family’s financial assets in order to get a clear picture of your financial status. Remember that it is okay to ask for help from loved ones or call your financial professional. Start with bank accounts and safety deposit boxes, retirement accounts, investment accounts, insurance policies, Social Security benefits, and any real estate. If you and your spouse did not have a trusted financial professional, now may be a good time to find one so that he or she may be able to help.

After you get a clear picture of your financial resources, the next step is to figure out how your income will operate within that financial framework. This step will be particularly important if you weren’t the primary breadwinner, or were not working.

Know What You Want

You may need to redefine what you want out of your life now—and what you want your life to look like in the future—then make a plan to work toward what you want to achieve. Retirement planning begins with a fresh review of your goals, income, and expenses.

Don’t be hasty with your financial decisions. Depending on your current needs and future plans, your financial portfolio may or may not need to shift. In most cases, your family’s financial portfolio is already set on a path to achieve the goals you and your spouse were working toward together. If you decide those goals—including where and when you want to retire—haven’t significantly changed, you’ll just need to make sure you’re still on track.

Let Experts Help

Female decision makers tend to be less risk tolerant and more focused on life goals.3 Financial professionals use their expertise to help you work toward financial independence or financial stability based on conversations about your life and what you want out of it. And, if you have financial questions, they can answer them.

READ MORE

1 “The Holmes-Rahe Stress Inventory,” The American Institute of Stress, accessed September 2022.

2 “Effect of Spousal Loss on Depression in Older Adults: Impacts of Time Passing, Living Arrangement, and Spouse’s Health Status before Death,” National Library of Medicine, December 2021.

3 “Women as the next wave of growth in US wealth management,” McKinsey, July 2020.

Pacific Life, its distributors, and respective representatives do not provide tax, accounting, or legal advice. The information above is provided for informational purposes only and should not be construed as investment, tax, or legal advice. Information is based on current laws, which are subject to change at any time. You should consult with your accounting or tax professionals for guidance regarding your specific financial situation.

Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products are issued by Pacific Life Insurance Company in all states except New York and in New York by Pacific Life & Annuity Company. Product availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

Pacific Life’s Home Office is located in Newport Beach, CA.

PL43A