Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

-

Individuals

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

-

Employers

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

-

Institutions

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

-

Financial Professionals & Brokers

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

These key factors can help you figure out your life insurance sweet spot.

When it comes to life insurance, almost everyone has the same question: How much do I need? While there’s no one-size-fits-all answer, there are some key factors that can help you determine what’s right for you and your family.

Most people overestimate how much life insurance costs and underestimate how much they need. This causes many people to be underinsured. Seven in 10 American consumers say they personally need more life insurance, according to the Life Insurance Marketing and Research Association (LIMRA). Many don’t have insurance at all, and among those who do, one in four only have employer-sponsored coverage, which is vulnerable to job changes. LIMRA estimates that even among the insured, 25 million Americans need more coverage.1

Most insured Americans (61%) report policies worth $100,000 or less (or were unsure of their coverage amount), according to MoneyGeek’s 2022 life insurance survey2. For many, this coverage falls far short of needs. In the U.S., the median salary is nearly $57,200, according the U.S. Bureau of Labor Statistics3. At that salary, a payout of less than $100,000 would cover less than two years of income replacement. By comparison, according to a general rule-of-thumb in the life insurance industry, life insurance should ideally cover ten times salary, plus some extra, such as $100,000 for each child.

To avoid a shortfall and get the amount of life insurance that’s right for your family, it’s important to understand your unique needs and situation.

What do I need life insurance for?

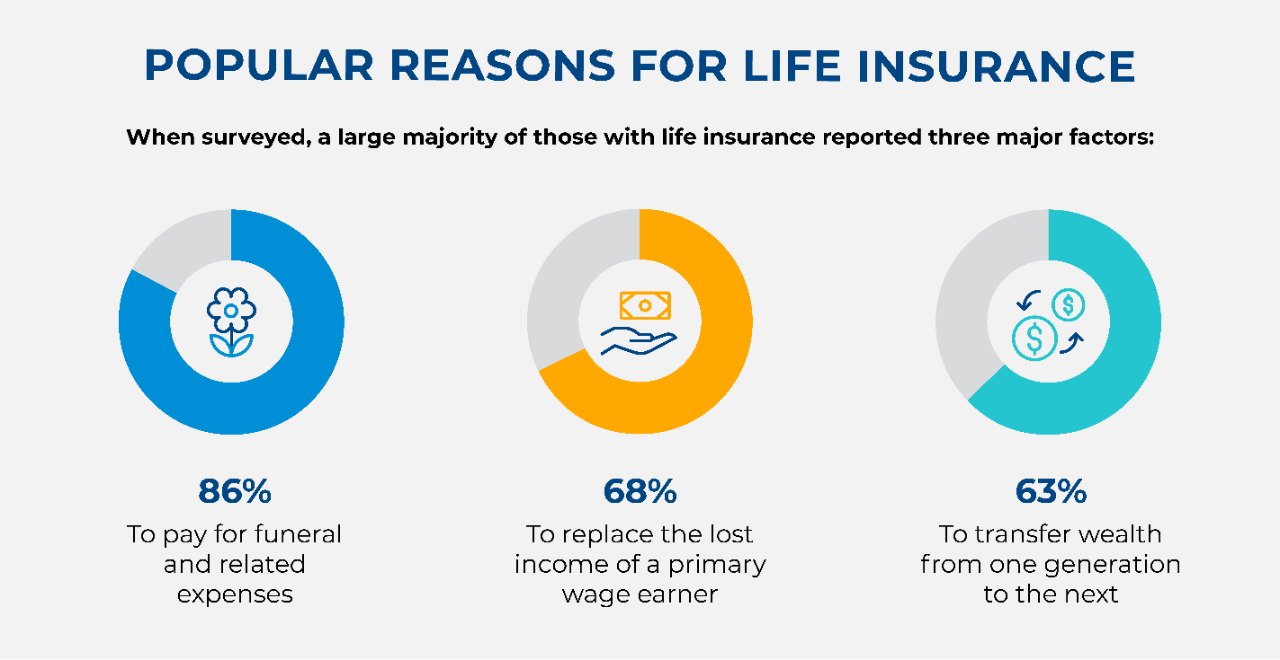

Life insurance helps provide security in a variety of situations, and it can help keep your family’s long-term goals on track for whatever happens.

- Almost half of American households (44%) would face significant financial difficulties if they lost the family’s primary wage earner, according to surveys by LIMRA4.

- More than a quarter (28%) of families would encounter serious financial trouble within the first month, LIMRA reports4.

For small business owners, it can help ensure the company’s continuity during times of transition.

Source: Life Insurance Marketing and Research Association (LIMRA)¹

Source: Life Insurance Marketing and Research Association (LIMRA)¹

How can I figure out the amount of life insurance I need?

To determine how much life insurance you need, start by calculating the financial obligations that you want to cover. This list can include a variety of commitments and goals that are unique to your situation. Some experts simplify this as the DIME method, which stands for debt, income, mortgage and education.

- Debt: Do you have outstanding non-mortgage debts that your family would be responsible for? This can include car loans, credit card debt and other large debts you may owe. It’s also worth noting funeral expenses, which can become an instant debt if not accounted for.

- Income Replacement: Do your loved ones rely on your ongoing income to maintain their current lifestyle? If so, you may want to consider a life insurance policy that includes some years of income replacement (how many years depends on the age of your children and other factors). Ultimately, it’s up to you to decide.

- Mortgage: Do you have a balance on your mortgage? Having life insurance pay off what you owe can help ensure that your family is able to stay in the same home.

- Education Spending: Do you have children or grandchildren who may someday attend college? If so, you may want to include future college costs in your calculations.

Once you’ve added up your DIME financial obligations, subtract any savings or assets that could be used for any of the above expenses. The resulting number is probably close to the right amount of life insurance coverage for you. This life insurance calculator from Pacific Life can help you get started. Work with a life insurance producer to help you with your unique financial goals.

READ MORE

Sources:

1 Life Insurance Marketing and Research Association (LIMRA), 2021 Insurance Barometer Study, accessed July 2023

2 MoneyGeek’s 2022 life insurance survey, accessed July 2023

3 U.S. Bureau of Labor Statistics, USUAL WEEKLY EARNINGS OF WAGE AND SALARY WORKERS SECOND QUARTER 2023, accessed July 2023

4 Life Insurance Marketing and Research Association (LIMRA), Why Life Insurance coverage is more important than ever, published February 2021, accessed July 2023

Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products can be issued in all states, except New York, by Pacific Life Insurance Company or Pacific Life & Annuity Company. In New York, insurance products are only issued by Pacific Life & Annuity Company. Product/material availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues. Insurance products and their guarantees, including optional benefits and any fixed subaccount crediting rates, are backed by the financial strength and claims-paying ability of the issuing insurance company. Look to the strength of the life insurance company with regard to such guarantees as these guarantees are not backed by the broker-dealer, insurance agency or their affiliates from which this product is purchased. Neither these entities nor their representatives make any representation or assurance regarding the claims-paying ability of the life insurance company.

Pacific Life, its affiliates, their distributors and respective representatives do not provide tax, accounting or legal advice. Any taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor or attorney.

The home office for Pacific Life & Annuity Company is located in Phoenix, Arizona. The home office for Pacific Life Insurance Company is located in Omaha, Nebraska.

PL72