Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

-

Individuals

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

-

Employers

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

-

Institutions

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

-

Financial Professionals & Brokers

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

How to reduce anxiety and bolster your retirement with reliable protected income.

Retirement can mean something different to everyone. But, for most, it includes the freedom to choose how you spend your time. It may also involve money-related stress when the reality of a decrease in income and rising healthcare costs set in.

Fortunately, if you are getting ready to retire or are newly retired, you can take steps now that may reduce your stress and help you live the retirement you want. One option you may want to consider is adding an annuity to your investment mix. That’s because annuities are one of the only ways you can generate protected lifetime income outside of Social Security or pensions.

What is an annuity?

An annuity is a financial product that can offer protected lifetime income and even the potential to grow your money. With an annuity, you make one or more payments to the insurance company. During the accumulation phase, your money has the opportunity to grow, tax deferred, which means you don’t pay taxes on earnings until you withdraw them. Once you’re ready to use that money — typically in retirement — you can switch to the income phase of the annuity and set up payments that can last for a period of time or for as long as you live. How much you receive will depend on your age and how much you contributed, along with other factors. You can even set up income that lasts as long as both you and your spouse live.

An annuity can provide:

- Reliable income. You can turn your annuity assets into a stream of income payments that is guaranteed and remains the same, regardless of what’s happening in the economy or the market.

- Tax-deferred growth. If your annuity allows your money to grow, any earnings will be tax deferred until withdrawn.

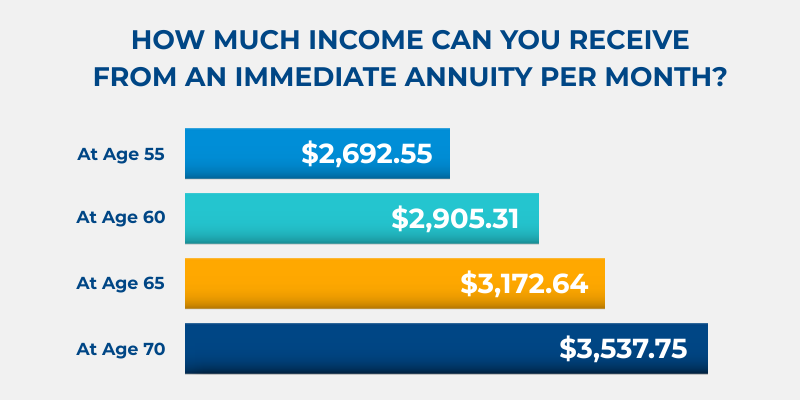

For illustrative purposes only. This example shows how much lifetime income you could receive from an immediate annuity if you paid a one-time, lump sum of $500,000, and started receiving income payments right away. Assumes a male annuitant purchases an immediate annuity with a payment of $500,000. Chart provides annuity payments beginning ages 55, 60, 65, and 70. Actual payout depends on your specific situation. Consult with your financial professional to find out how an annuity could work for your situation. Pacific Life, Aug 2023.

For illustrative purposes only. This example shows how much lifetime income you could receive from an immediate annuity if you paid a one-time, lump sum of $500,000, and started receiving income payments right away. Assumes a male annuitant purchases an immediate annuity with a payment of $500,000. Chart provides annuity payments beginning ages 55, 60, 65, and 70. Actual payout depends on your specific situation. Consult with your financial professional to find out how an annuity could work for your situation. Pacific Life, Aug 2023.

Security Instead of Stress

For nearly 1 in 2, the number one financial concern of adults age 55 and older is not having enough money saved for retirement, according to SeniorLiving.org1. In addition, NASDAQ reports that 66% of Americans are worried they will run out of money in retirement2.

Financial worries like these may be caused by the uncertainty you face when you no longer have predictable income through an employer. By adding an annuity to your overall retirement plan, you may be including a remedy that most other financial products can’t provide: the security of protected lifetime income.

In fact, the Secure Retirement Institute found that over two-thirds (69 percent) of retirees who own an annuity have confidence that they’ll be able to live the retirement lifestyle they want3. This confidence level was much higher than those without an annuity.

What Can Protected Income Do For You?

Having a steady stream of income can help you create the retirement you’ve always imagined. This might include travel, hobbies, spending more time with friends and family, providing financial support for loved ones, expanding charitable donations, or other pursuits. Annuities can play a role in helping you create the vision and enjoy the retirement you want.

Learn more about Pacific Life annuities.

READ MORE

All guarantees are subject to the claims-paying ability and financial strength of the issuing insurance company and do not protect the value of the variable investment options, which are subject to market risk.

Under current law, a nonqualified annuity that is owned by an individual is generally entitled to tax deferral. IRAs and qualified plans—such as 401(k)s and 403(b)s—are already tax deferred. Therefore, a deferred annuity should be used only to fund an IRA or qualified plan to benefit from the annuity’s features other than tax deferral. These features include lifetime income, death benefit options, and the ability to transfer among investment options without sales or withdrawal charges.

No bank guarantee • Not a deposit • Not FDIC/NCUA insured • May lose value Not insured by any federal government agency

Sources:

1 SeniorLiving.org, Top 10 Fears of Older Adults in 2023, published May, 2023, accessed July 2023

2 NASDAQ, 66% of Americans Are Worried They’ll Run Out of Money in Retirement — Here Are 7 Tips To Make Sure That Doesn’t Happen, published December 2022, accessed July 2023

3 Secure Retirement Institute, SRI Study: Owning An Annuity Increases Retirement Confidence, published June 2021, accessed July 2023

Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products can be issued in all states, except New York, by Pacific Life Insurance Company or Pacific Life & Annuity Company. In New York, insurance products are only issued by Pacific Life & Annuity Company. Product/material availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

Insurance product and rider guarantees, including optional benefits and any fixed crediting rates or annuity payout rates, are backed by the financial strength and claims-paying ability of the issuing insurance company and do not protect the value of the variable investment options. They are not backed by the broker/dealer from which this annuity is purchased, by the insurance agency from which this annuity is purchased, or any affiliates of those entities, and none makes any representations or guarantees regarding the claims-paying ability of the issuing insurance company. The home office for Pacific Life & Annuity Company is located in Phoenix, Arizona.

The home office for Pacific Life & Annuity Company is located in Phoenix, Arizona. The home office for Pacific Life Insurance Company is located in Omaha, Nebraska.

PL73