Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

-

Individuals

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

-

Employers

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

-

Institutions

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

-

Financial Professionals & Brokers

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

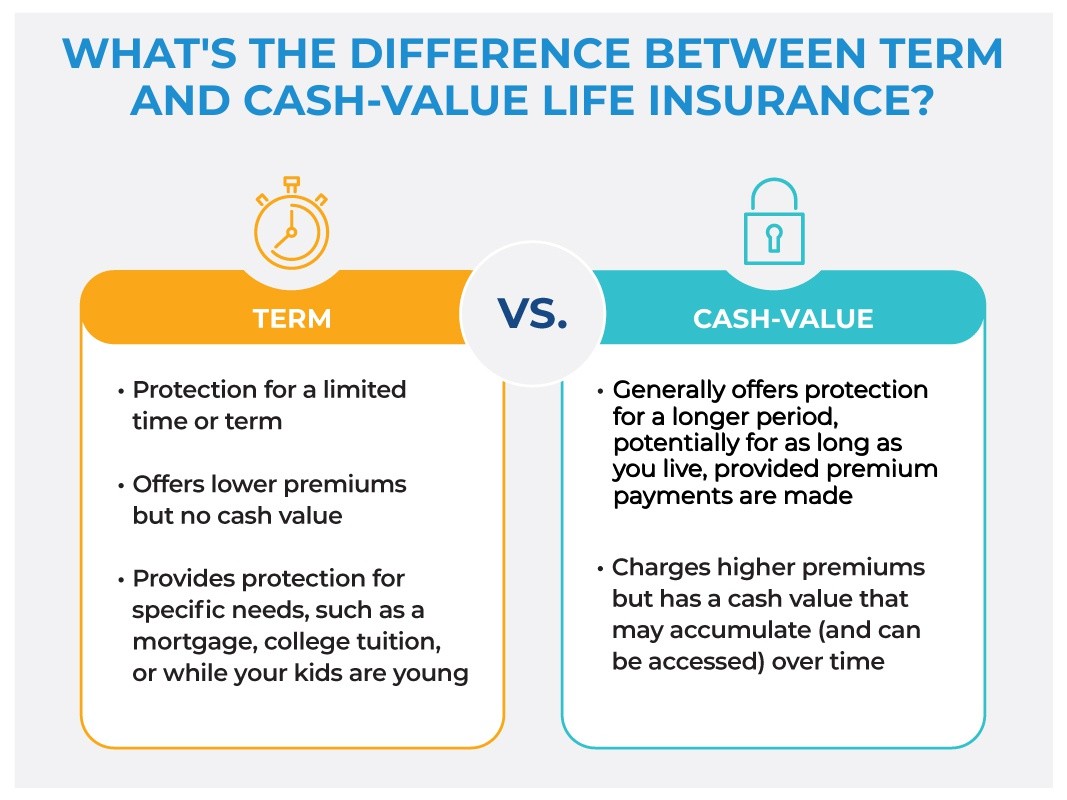

If you’re in the market for life insurance protection, don’t overlook cash-value life policies.

There are two main types of life insurance: term and cash-value. While term policies are typically more popular, simply because they offer life insurance protection for less money, cash-value policies have additional benefits you may want to consider.

What’s the difference between term and cash-value life insurance?

Like its name, term life insurance provides temporary protection for a specific term or time period — most often 10, 15, or 20 years. Once that term is over, you’re no longer covered by the life insurance policy. You may be able to renew the policy, but because you’re older, your premiums will likely increase.

A cash-value life insurance policy, on the other hand, offers lifetime protection, as long as you continue to pay your premiums. In addition, cash-value life insurance gives you the potential to build cash value that you may be able to access later, to use for unexpected expenses, long-term care costs, or help supplement your retirement income. In short, while cash-value policies typically cost more than term policies, they offer more flexibility to be used in different ways.

Benefits of cash-value life insurance

While the death benefit for both term and cash-value life insurance is paid to the beneficiary free of income tax1, cash-value life insurance has other benefits that you won’t get with a term policy.

- Cash value — Each time you pay premiums, a portion of that money goes toward the policy’s cash value. This cash value grows at a rate specific to the type of policy and how the policyowner directs the cash value to be allocated.. With some types of cash-value life insurance policies, you have the ability to select the investment options that drive your cash value’s potential growth (or loss). In other types of policies, like whole life, the insurance company sets the growth rate for the cash value. Either way, any cash value growth is tax deferred, so you won’t pay current taxes on interest that builds up within the account.

- Stable premiums — Unlike term life insurance premiums, which will increase at renewal, permanent life insurance premiums will generally stay the same for as long as you own the policy, contingent upon the performance of the policy.

- Flexibility to tailor the policy to your needs — Cash-value life insurance often offers what are called riders3, or additions to the policy, that let you customize it to meet your needs. For example, you may add a Long-Term Care, Chronic Illness, or Critical Illness rider to your policy, which can allow you to use the death benefit to pay for health care costs if you are diagnosed with a certain illness or need long-term care.

Uses for cash-value life insurance

If you’re looking for short-term life insurance to protect your family just for as long as you need to pay off a mortgage, get your kids through college, or pay off student loans, then less expensive term life insurance may be a better fit for you. However, if you have significant financial obligations that are not time sensitive, such as protecting your legacy for your children, you might want to consider a cash-value life insurance policy.

Besides providing a tax-advantaged death benefit, cash-value life insurance can be used to:

- Paying estate taxes — If you are leaving your beneficiaries a large enough estate, they may have to pay estate taxes on their inheritance2. Proceeds from cash-value life insurance can be used to offset those taxes and help maximize the amount you leave your heirs.

- Help supplement your retirement income — Consider taking withdrawals or loans from your policy’s cash value to pay for retirement expenses4.

There are a number of different kinds of cash-value life insurance policies, each with their own features, benefits and considerations. Talk to your financial professional to see if a cash-value life insurance policy may be right for you.

READ MORE

1 For federal income tax purposes, life insurance death benefits generally pay income tax-free to beneficiaries pursuant to IRC Sec. 101(a)(1). In certain situations, however, life insurance death benefits may be partially or wholly taxable. Situations include but are not limited to: the transfer of a life insurance policy for valuable consideration unless the transfer qualifies for an exception under IRC Sec. 101(a)(2) (i.e. the transfer-for-value rule); arrangements that lack an insurable interest based on state law; and an employer-owned policy unless the policy qualifies for an exception under IRC Sec. 101(j).

2 As of September 2024, the estate tax exemption is $13.61M per individual; source: IRS, retrieved September 2024

3 Riders will likely incur additional charges and are subject to availability, restrictions and limitations. When considering a rider, request a life insurance policy illustration from your life insurance producer to see the rider’s impact on your policy’s values.

4 Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits.

Benefits paid by accelerating the policy’s death benefit may or may not qualify for favorable tax treatment under Section 101(g) of the Internal Revenue Code of 1986. Tax treatment of an accelerated death benefit may depend on factors such as life expectancy at the time benefits are accelerated, the amount of benefits, the amount of qualified expenses incurred, or if similar benefits are being received under other contracts. Receipt of accelerated death benefits may affect eligibility for public assistance programs such as Medicaid. When benefits are received from multiple policies providing long-term care or chronic illness benefits for a given insured, including policies with different owners, all of those benefits must be aggregated to determine their taxability. Tax laws relating to accelerated death benefits are complex. Pacific Life cannot determine whether the benefits are taxable. Clients are advised to consult with qualified and independent legal and tax advisor for more information.

In order to sell life insurance, a financial professional must be a properly licensed and appointed life insurance producer.

Pacific Life, its affiliates, their distributors and respective representatives do not provide tax, accounting or legal advice. Any taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor or attorney.

Life insurance is subject to underwriting and approval of the application and will incur monthly policy charges. In general, additional premium is required to continue coverage of the policy. Policy may lapse if premium is insufficient to continue coverage.

Pacific Life is a product provider. It is not a fiduciary and therefore does not give advice or make recommendations regarding insurance or investment products.

Pacific Life refers to Pacific Life Insurance Company and its subsidiary Pacific Life & Annuity Company. Insurance products can be issued in all states, except New York, by Pacific Life Insurance Company and in all states by Pacific Life & Annuity Company. Product/material availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

The home office for Pacific Life & Annuity Company is located in Phoenix, Arizona. The home office for Pacific Life Insurance Company is located in Omaha, Nebraska.

PL79