Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

-

Individuals

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

-

Employers

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

-

Institutions

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

-

Financial Professionals & Brokers

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

Thinking beyond basic retirement planning can give you greater financial flexibility in your golden years.

Your retirement strategy should begin with a tax-advantaged retirement account, but it doesn't have to end there. Supplementing your 401(k) or IRA with cash value life insurance can help give you greater financial flexibility during your lifetime while providing protection to your loved ones.

Unlike term life insurance, which only pays out a death benefit, cash value life insurance allows you to allocate your premiums inside the policy and gives you access to its available cash value while you’re alive. Cash value life insurance can also offer tax advantages that can benefit both you and your family.

Here are four ways cash value life insurance can enhance your retirement strategy:

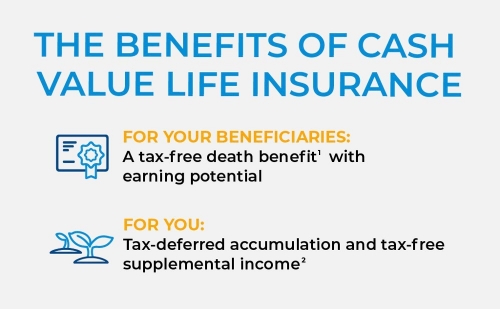

1. Protection for loved ones

A cash value life insurance policy pays a tax-free death benefit1 to your beneficiaries at your death. Your family can use the policy death benefit in any way they wish. For instance, it may help with expenses such as day-to-day living costs or paying down a mortgage.

2. Tax-deferred growth potential

Cash value policies offer tax-deferred growth potential—giving you another vehicle you can use to invest toward the future. When you purchase a cash value life insurance policy, part of your premium is allocated into an investment option that can accumulate tax-deferred interest over time. This option may be especially appealing if you contribute the maximum annual amount to your retirement accounts and are looking for further tax-deferred growth opportunities.

3. Tax-free supplemental income potential2

Cash value life insurance offers the ability to access the available cash value through potentially tax-free2 loans or withdrawals. Such loans or withdrawals may help you and your family cover unexpected expenses before or during your retirement.

4. Risk management

A cash value life insurance policy may help diversify your financial portfolio, potentially reducing your portfolio’s overall volatility and risk of loss depending on the type of cash value life insurance you choose. What's more, some policies allow you to allocate money to indexed accounts that credit interest based in part on the performance of major stock market indexes.3 The interest rate credited for these accounts is protected from falling below a set level, which means your policy’s cash value is protected from market-based losses. Your cash value will be reduced only by policy charges and any loans, withdrawals, or other distributions you take from the policy.

If you're looking for a tool that protects your family in the event of the unexpected while also serving as a source of potentially tax-free2 supplemental retirement income, consider looking into a cash value life insurance policy. Work with a professional life insurance producer to help you find the product that best fits your situation and goals.

READ MORE

1 For federal income tax purposes, life insurance death benefits generally pay income tax-free to beneficiaries pursuant to IRC Sec. 101(a)(1). In certain situations, however, life insurance death benefits may be partially or wholly taxable. Situations include, but are not limited to: the transfer of a life insurance policy for valuable consideration unless the transfer qualifies for an exception under IRC Sec. 101(a)(2) (i.e. the transfer-for-value rule); arrangements that lack an insurable interest based on state law; and an employer-owned policy unless the policy qualifies for an exception under IRC Sec. 101(j).

2 For federal income tax purposes, tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death (any outstanding policy debt at time of lapse or surrender that exceeds the tax basis will be subject to tax); (3) withdrawals taken during the first 15 policy years do not cause, occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC §§ 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits.

3 Indexed universal life insurance products do not directly participate in any stock or equity investment.

The results and explanations generated by the calculator on this page may vary due to user input and assumptions. This information may not be used to project or predict future results. Pacific Life does not guarantee the accuracy of the calculations, results, explanations, nor applicability to your specific situation. we recommend that you use this tool as a guideline only and ultimately see the guidance of an experience professional. CalcXML, the provider of this information and interactive calculator, is an independent third-party and it not affiliated with Pacific Life.

The information above, including the results and explanations generated by the calculator, is provided for informational purposes only and should not be construed as investment, tax, or legal advice. Information is based on current laws, which are subject to change at any time. You should consult with their accounting or tax professionals for guidance regarding your specific financial situation.

Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products are issued by Pacific Life Insurance Company in all states except New York and in New York by Pacific Life & Annuity Company. Product availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

Pacific Life’s Home Office is located in Newport Beach, CA.

PL33A