Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

-

Individuals

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

-

Employers

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

-

Institutions

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

-

Financial Professionals & Brokers

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

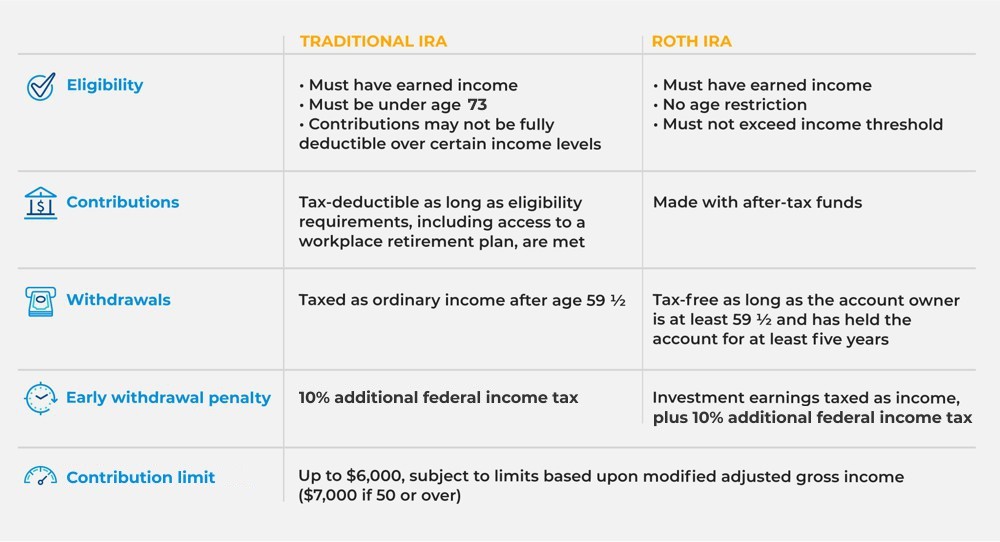

Understanding the difference between a traditional and Roth IRA can go a long way in planning your retirement savings strategy.

Being able to live the lifestyle you want in retirement often depends on saving consistently over many years. An individual retirement account (IRA) can be a powerful tool in this effort. Most IRAs offer tax benefits that encourage long-term retirement savings, along with a variety of investment options, including mutual funds and annuities.

The most common types of IRAs held by individual investors are traditional IRAs and Roth IRAs. Here’s what you need to know about each type of retirement account to help you determine which may be best for you.

Traditional IRAs

With a traditional IRA, you may be eligible for a tax deduction on some or all of the contributions you make each year, assuming you meet eligibility requirements. In practical terms, this means both income taxes on the money you use to fund your account and taxes on any gains in your portfolio invested in your IRA are delayed until they are withdrawn.

If you wait to withdraw funds until you turn age 59½, the IRS will tax your withdrawals as ordinary income. If you withdraw your money earlier, however, you may owe an additional 10% federal income tax. Additional taxes may be exempt for qualifying events. For example, withdrawals up to a certain amount for buying your first home or to cover death, disability or certain medical expenses.

Roth IRAs

Roth IRAs differ from traditional IRAs in one key way: The contributions you make to a Roth account are with money that has already been taxed. The benefit to this setup comes later, during retirement, when you can withdraw your retirement savings tax-free.

There are a couple additional caveats with Roth IRAs. First, to qualify for tax-free withdrawals, you need to hold your investments in a Roth IRA for more than five years. Second, the IRS limits the amount you can contribute to a Roth IRA if your taxable earnings exceed its contribution limits in a given year; some taxpayers with high taxable income will not be able to contribute at all. Third, Roth IRAs impose the same additional 10% federal income tax for withdrawals before age 59½ as do traditional IRAs. With a Roth IRA, however, you’ll also have to pay taxes on any investment earnings if you make an early withdrawal that’s not covered by one of the exemptions mentioned above.

Which is right for you?

The major difference between traditional and Roth IRAs involves when you pay taxes. Looking at your income today and comparing it to what you expect to receive in retirement could help you choose the right type of account.

For example, if you expect your income in retirement to be lower than it is now, you might consider a traditional IRA to shelter some of your current income from taxes. In this scenario, your withdrawals in retirement would likely be taxed at a lower rate, too.

Conversely, if you’re early in your career, a Roth IRA may help you stretch your future retirement savings. If years of compound growth result in significant investment gains, tax-free withdrawals could represent a substantial savings over a traditional IRA.

Since investments and taxes can be difficult to predict, you should consult a financial professional to discuss whether a Roth or traditional IRA would be a good fit for your particular financial needs.

READ MORE

Pacific Life, its distributors, and respective representatives do not provide tax, accounting, or legal advice.

The above is provided for informational purposes only and should not be construed as investment, tax, or legal advice. Information is based on current laws, which are subject to change at any time. You should consult with your accounting or tax professionals for guidance regarding your specific financial situation.

Pacific Life is a product provider. It is not a fiduciary and therefore does not give advice or make recommendations regarding insurance or investment products.

Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products are issued by Pacific Life Insurance Company in all states except New York and in New York by Pacific Life & Annuity Company. Product availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

Pacific Life’s Home Office is located in Newport Beach, CA.

PL36A