Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

-

Individuals

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

-

Employers

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

-

Institutions

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

-

Financial Professionals & Brokers

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

Take these steps to help your loved ones prepare financially in the event the worst happens to you.

The unexpected death of a spouse or parent is emotionally devastating for those left behind. Add in the financial implications of losing the family’s main income earner and it can be downright terrifying for those left behind.

Each family is unique, and a family’s individual circumstances dictate the severity of the financial impact of the death of a breadwinner. The family’s overall financial picture is influenced by multiple factors, such as whether the family is a one- or two-income household, whether the breadwinner is a single parent or part of a blended family, whether young children are left behind (and whether those children have special needs), and how much debt the family carries.

No matter your family situation, you can plan ahead for financial protection. While no one likes to think about the possibility of an unanticipated loss, having these protections in place can be a great comfort in the event the worst happens.

Purchase adequate life insurance

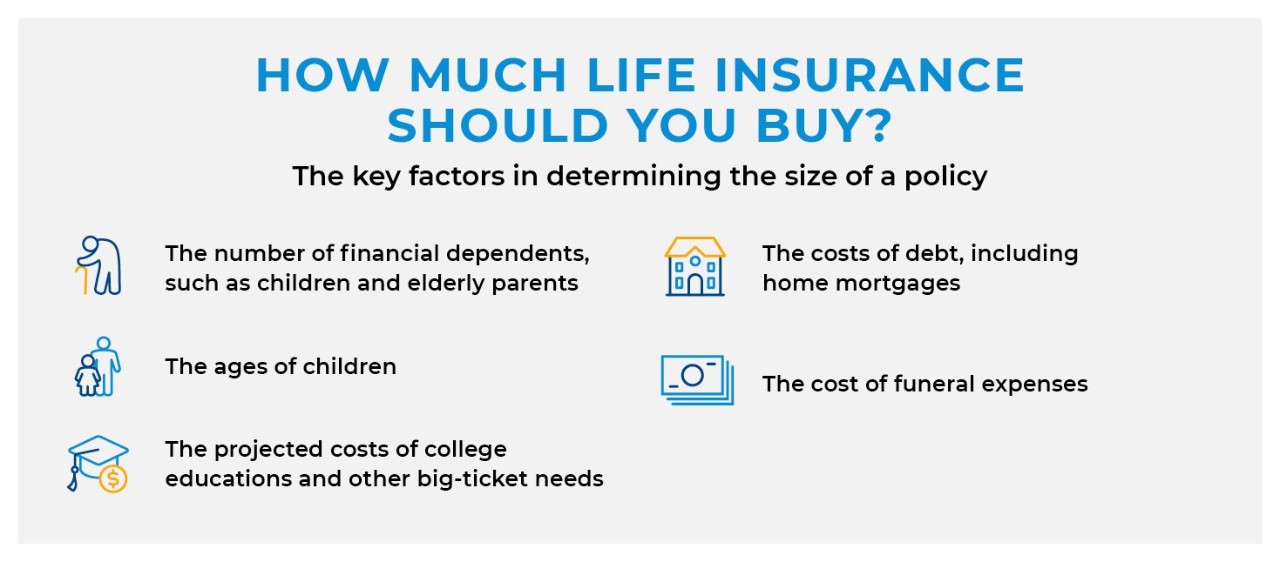

Conventional wisdom suggests purchasing a life insurance policy equal to 10 times the breadwinner’s annual income. But that multiple can shift depending on your age, the ages of your spouse and any children, how much debt the family has, as well as any other special circumstances. For example, if the breadwinner is also financially supporting aging family members, a larger policy may be needed. Likewise, business owners who anticipate that their company will grow or who expect to contribute to their surviving family members income should take these projections into consideration as they choose an appropriate level of life insurance coverage.

As you’re deciding what level of coverage your family would need in the event of your death, consider the following questions:

- Could your policy cover any existing debt, such as a mortgage?

- If you have children, how many years will it be until they reach adulthood?

- Do you need enough coverage to pay for your children’s education

- Do you want your insurance to cover funeral expenses?

For two-parent households in which one parent stays at home with the kids, don’t forget to cover the stay-at-home spouse. While they may not be earning a paycheck, if they died, your family would still need to offset the cost of childcare and household help.

Make sure beneficiaries are up-to-date

Any time your family experiences a significant lifestyle change like a birth, marriage or divorce, it’s crucial to update the beneficiaries on life insurance policies and retirement accounts. If either you or your spouse have been married before, this step is particularly crucial; there have been several notable cases in which people died before updating their beneficiaries, leaving a former spouse to inherit assets rather than the current spouse or children.

Stay on top of estate planning

Similarly, it’s important to periodically update your will and any trusts you may have in place. Family situations, estate tax laws and even your preferences for charitable giving might shift over time.

One aspect of estate planning that is sometimes overlooked is centralizing all your important financial and legal documents, as well as information like account numbers and passwords on all financial accounts and insurance policies. Having this information organized and stored safely can make it easier for those left behind.

Dealing with financial stress in the wake of a loved one’s unexpected death is a heavy load to carry. Work with your attorney and financial professional to develop plans now that can provide an immense gift to those you love most.1

READ MORE

1 Remember, in order to sell life insurance, a financial professional must be a properly licensed and appointed life insurance producer.

Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products are issued by Pacific Life Insurance Company in all states except New York and in New York by Pacific Life & Annuity Company. Product availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

Pacific Life’s Home Office is located in Newport Beach, CA

PL14A