Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

-

Individuals

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

-

Employers

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

-

Institutions

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

-

Financial Professionals & Brokers

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

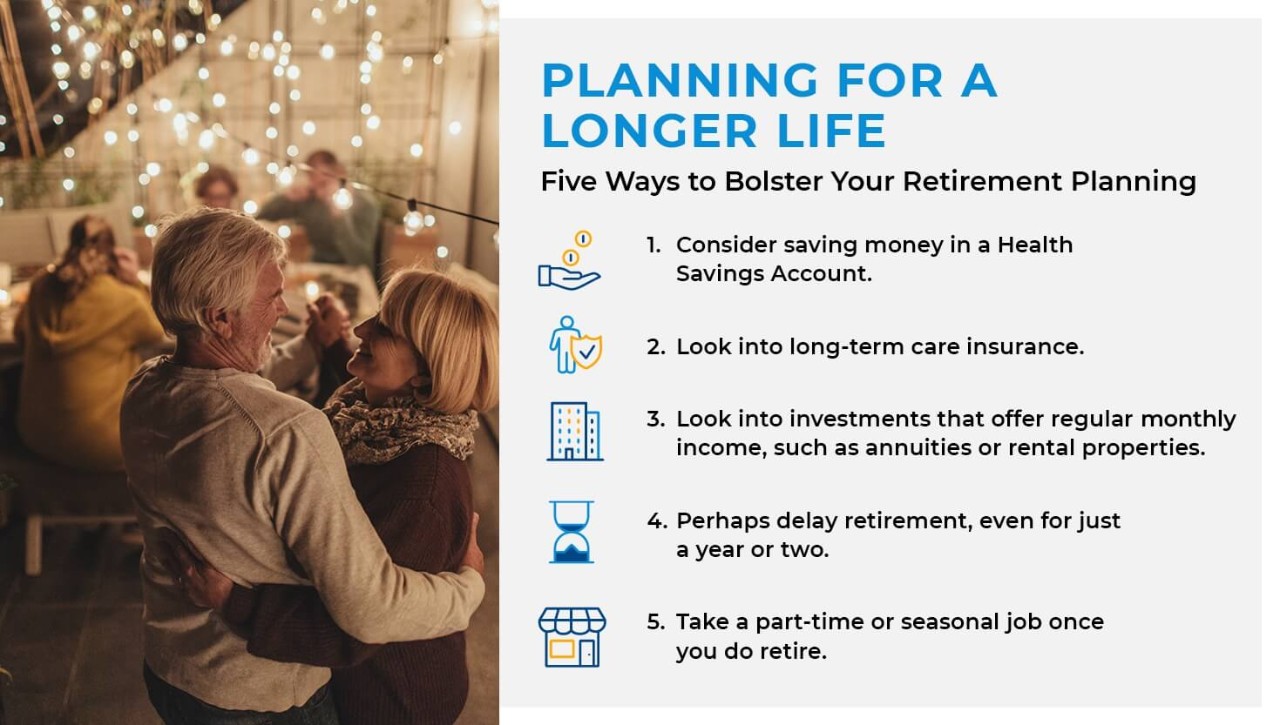

The good news: Retirees are living longer. The bad news: That may mean retirees will have to fund more years of retirement.

While increasing longevity is welcome, funding more years in retirement may present some financial challenges. Here are some things to keep in mind as you plan for a long retirement.

Understanding the three phases of retirement

Increasing life expectancy means your retirement could last 30 years or more. With this significant time horizon, retirement isn’t just a static state; instead, it may consist of three distinct phases, each with its own financial implications.

While many anticipate spending less in retirement, the first decade of retirement often brings a period of increased spending. In the first 10 years or so, it’s common for retirees to spend time and money on travel and other hobbies they didn’t have time for while working.

After pursuing these adventures, retirees tend to become less active and more family focused in the second decade of retirement. It’s also common for retirees to begin encountering health problems that keep them home more. Spending tends to decrease, as retirees spend less on travel and entertainment, and many decide to downsize their homes.

The third decade of retirement is often a period when health tends to decline, leading to even less discretionary spending, though health-related costs often rise.

Thinking about retirement as a long period with different parts can help you create a realistic plan that accounts for the possibility of increased spending immediately postretirement while preserving a healthy amount of savings to cover rising health-care costs down the road.

Planning for health care

In fact, the cost of health care in retirement presents one of the biggest unknowns for retirees. While Medicare will cover a portion of your medical expenses, you’ll need to consider out-of-pocket medical expenses as you fund your retirement, especially since Medicare does not cover the cost of long-term care.

Consider saving money in a health savings account if you’re eligible, investigating long-term care options and keeping on top of preventive health care now—all of which can help address your health-care costs in retirement.

Regulating your retirement income

To buffer the dips and spikes in your postretirement spending, you may want to consider strategies to provide steady income streams beyond your Social Security benefits. Consider such investments as annuities that offer regular guaranteed income or rental properties that may provide you with cash flow. Some people are also reconsidering a total retirement, especially early on. Launching an encore career in a field you’re passionate about or taking a part-time or seasonal job can give your retirement savings more time to accumulate and provide satisfaction and fulfillment along the way.

Living in an era of improving medical technology and longevity means you may be able to enjoy retirement longer than you think. By creating strategies to address the financial challenges of each stage of retirement, you’ll be able to reap the rewards of all your hard work and planning.

READ MORE

The results and explanations generated by this calculator may vary due to user input and assumptions. Pacific Life does not guarantee the accuracy of the calculations, results, explanations, nor applicability to your specific situation. We recommend that you use this calculator as a guideline only and ultimately seek the guidance of an experienced professional. CalcXML, the provider of this information and interactive calculator, is an independent third-party and is not affiliated with Pacific Life.

This material is not intended to be used, nor can it be used by any taxpayer, for the purpose of avoiding U.S. federal, state or local tax penalties. This material is written to support the promotion or marketing of the transaction(s) or matter(s) addressed by this material. Pacific Life, its affiliates, their distributors and respective representatives do not provide tax, accounting or legal advice. Any taxpayer should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor or attorney.

Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products are issued by Pacific Life Insurance Company in all states except New York and in New York by Pacific Life & Annuity Company. Product availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues. Insurance products and their guarantees, including optional benefits and any crediting rates, are backed by the financial strength and claims-paying ability of the issuing insurance company. Look to the strength of the life insurance company with regard to such guarantees as these guarantees are not backed by the broker-dealer, insurance agency or their affiliates from which products are purchased. Neither these entities nor their representatives make any representation or assurance regarding the claims-paying ability of the life insurance company.

Pacific Life’s Home Office is located in Newport Beach, CA.

PL8A