Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

-

Individuals

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

-

Employers

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

-

Institutions

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

-

Financial Professionals & Brokers

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

These four steps can help you choose the best protection for you and your family.

Life insurance is a valuable safeguard for a beneficiary’s financial position and can give you, as the policyowner, peace of mind. Certain types can help boost your financial strength as you head into your retirement years. If you have questions about which type to buy, how much coverage you need, and how life insurance can play a key role in your retirement income strategy, speak to your financial professional about your options first. In addition, the following four steps can help you determine the best option for your needs:

1. Determine your goal.

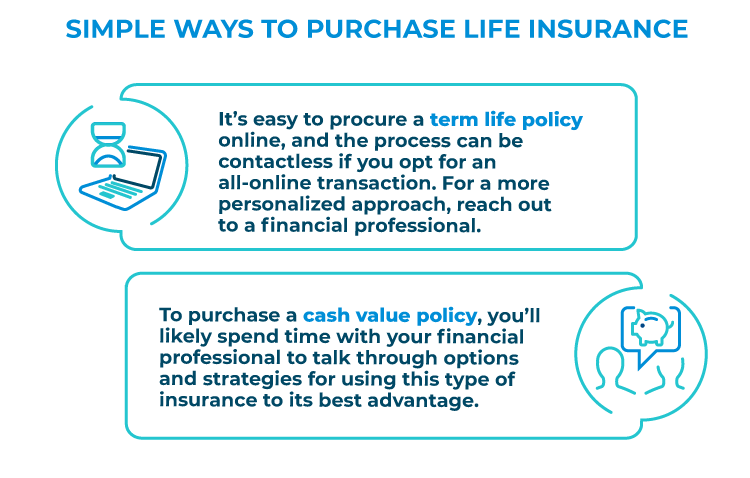

If financial protection for your family, property, or business in the event of your premature death is your primary goal, term life insurance may be a good option. It protects for a certain period of time—such as 10, 20, or 30 years—at affordable premium costs.

If you are looking for a longer period of protection and additional benefits you can access while you are still living, consider cash value policies. These policies offer a tax-free1 death benefit for your beneficiaries (i.e. loved ones) plus tax-deferred growth potential and tax-free supplemental income2 through withdrawals and policy loans from the available accumulated cash value. Because the premiums for cash value life insurance are generally higher than term life insurance, the typical purchaser is someone who is willing to pay more for the tax advantages and additional features of cash value policies for policyowners and/or involve estate-planning strategies that may reduce potential estate tax burdens on survivors.

Some term life insurance policies have an option to convert to a cash value policy before the term is up, saving you the hassle of having to go through the underwriting process again. If that’s something you’re interested in, make sure to inquire about that option with your financial professional.

2. Evaluate your coverage need.

While you may have heard of such rules of thumb as a certain multiple of your current income, your need will vary based on your unique financial condition. Explore our easy-to-use online calculators to help you determine how much coverage you may need.

3. Learn how your health may impact your policy options.

You may wonder how much health information you’ll have to divulge—or whether you’ll have to make a trip to the doctor—to purchase life insurance. The process for evaluating a customer’s life insurance request may simply rely on existing medical records and an online form, while other methods may require treadmill tests, blood draws, and months of processing.

Many carriers offer simplified underwriting programs for a less invasive and contactless process.

4. Consider company credentials and reputation.

You want your provider to be in business for the long term so it can honor your policy when the time comes. Pacific Life was established nearly 160 years ago. It received the top spot on the Forbes Advisor 2020 list of best insurance companies3. Pacific Life scored highest in the rankings, thanks to a substantial portion of its cash value life insurance products scoring 5 stars from Veralytic, and 85% of its products scoring 4 stars or better3. In 2021, the company’s life insurance division also received an Insurance Service Award by DALBAR, the third year it was recognized for superior customer service4. The company also receives top ratings from independent ratings agencies, landing the company in the top 7 percent of life insurance companies with its Comdex Score of 93%5.

READ MORE

1 For federal income tax purposes, life insurance death benefit proceeds paid in a lump sum generally pay income tax-free to beneficiaries pursuant to IRC Sec. 101(a)(1). In certain situations, however, life insurance death benefits may be partially or wholly taxable. Situations include, but are not limited to: the transfer of a life insurance policy for valuable consideration unless the transfer qualifies for an exception under IRC Sec. 101(a)(2) (i.e. the “transfer-for-value rule”); arrangements that lack an insurable interest based on state law; and an employer-owned policy unless the policy qualifies for an exception under IRC Sec. 101(j). When otherwise income tax-free death benefit proceeds are paid in a series of payments after death, a level percentage of each payment is taxable as interest income.

2 For federal income tax purposes, tax-free income assumes, among other things: (1) withdrawals do not exceed tax basis (generally, premiums paid less prior withdrawals); (2) policy remains in force until death (any outstanding policy debt at time of lapse or surrender that exceeds the tax basis will be subject to tax); (3) withdrawals taken during the first 15 policy years do not cause, occur at the time of, or during the two years prior to, any reduction in benefits; and (4) the policy does not become a modified endowment contract. See IRC §§ 72, 7702(f)(7)(B), 7702A. Any policy withdrawals, loans and loan interest will reduce policy values and may reduce benefits.

3 "The Best Life Insurance Companies 2021", Forbes Advisor, Jan 2021

4 Pacific Life Wins 2020 DALBAR Insurance Service Award, Pacific Life, Feb. 2021

5 Pacific Life Insurance Ratings & Financials, Pacific Life, Mar. 2021

According to the Tax Cuts and Jobs Act of 2017, the federal estate, gift and generation-skipping transfer (GST) tax exemption amounts are all $10,000,000 per person (indexed for inflation effective for tax years after 2011); the maximum estate, gift and GST tax rates are 40%. In 2026, the federal estate, gift and generation-skipping transfer (GST) tax exemption amounts are scheduled to revert to $5,000,000 per person (indexed for inflation for tax years after 2011).

The information represented in the calculator above, including the results and explanations generated by the calculator, is provided for informational purposes only and should not be construed as investment, tax, or legal advice. Information is based on current laws, which are subject to change at any time. You should consult with their accounting or tax professionals for guidance regarding your specific financial situation.

Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products are issued by Pacific Life Insurance Company in all states except New York and in New York by Pacific Life & Annuity Company. Product availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

Pacific Life’s Home Office is located in Newport Beach, CA.

PL61