Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

-

Individuals

Discover financial solutions that protect your future and provide peace of mind. Whether you're exploring annuities, life insurance, or understanding employee benefits through your workplace, Pacific Life offers resources and products designed to meet your personal and family goals.

-

Employers

Support your workforce with innovative employee benefits and retirement solutions. Pacific Life partners with business owners, benefits administrators, and pension fund managers to create customized programs that attract and retain top talent while securing their financial future.

-

Institutions

Simplify complex retirement and pension risk management with our tailored solutions for large organizations. Pacific Life specializes in working with institutions to address their unique challenges, offering expertise in pension de-risking and strategic retirement planning for a more secure future.

-

Financial Professionals & Brokers

Empower your clients with confidence by leveraging Pacific Life’s comprehensive portfolio of financial products. From annuities to life insurance, we provide the tools, resources, and support to help financial advisors and brokers deliver exceptional value and long-term results.

The first in our continuing conversation on retirement income | June 2026

Authors

| Christine BassHead of Defined Contribution Lifetime Income |

| Dr. Qi SunFinancial Economist |

Over the past several decades, well-documented shifts in employer-sponsored retirement plans from defined benefit to defined contribution structures have placed greater responsibility on individual plan participants to make saving and investment decisions, even as plan fiduciaries continue to play a critical role in shaping plan design, investment menus, and default strategies intended to support long-term retirement outcomes. To assist participants, many of whom lack financial expertise, the retirement ecosystem has largely emphasized plan design and investment solutions aimed at improving accumulation outcomes—including automatic enrollment, automatic contribution escalation, and qualified default investment alternatives (QDIAs)—with a general focus on maximizing retirement account balances and returns.

However, retirement risk is not solely about maximizing account balances or managing market-related risks. It also concerns whether accumulated assets can be translated into reliable income over an uncertain lifetime to support a participant's consumption needs throughout retirement.

In addition to sustaining consumption, retirement planning must also address other objectives that arise during retirement, such as:

- providing for health-related and long-term care needs,

- maintaining flexibility to absorb unexpected expenses, and

- preserving assets for bequests.

Account values and returns provide useful information about retirement preparedness, but on their own they offer an incomplete view of how effectively assets translate into sustainable income over retirement. As Robert Merton noted in The Crisis in Retirement Planning (2014),1 focusing on market-related risk alone can obscure other important income-oriented risks as “an investment [that] is risk-free from the asset value standpoint, may be very risky in income terms.” This distinction becomes evident when comparing how assets behave when evaluated through a longer-term, income-oriented lens rather than short-term price movements. For example, long-duration assets such as annuities or long-tenor fixed income securities may exhibit significant price volatility as interest rates change, yet can provide relatively stable income when held to support consumption needs over an extended time horizon or lifetime.

Taken together, these considerations suggest that a central challenge in retirement planning lies both in generating returns and in effectively aligning accumulated assets with future income needs over an indeterminate retirement horizon; specifically, matching future income liabilities with assets in the presence of longevity-dependent timing. When retirement outcomes are evaluated through an income lens rather than solely through an asset value lens, the nature of risk expands to include how reliably different income needs can be met over time. From a consumption perspective, future income needs vary in purpose, flexibility, and risk exposures, indicating that different types of income liabilities may warrant different governance frameworks and income generation strategies. As the retirement income landscape evolves, these challenges point to the need for a framework that moves beyond the retirement planning strategies of today and instead organizes around the strategies of tomorrow which consider the nature of meeting future income needs.

| A central challenge in retirement planning lies both in generating returns and in effectively aligning accumulated assets with future income needs over an indeterminate retirement horizon; specifically, matching future income liabilities with assets in the presence of longevity-dependent timing. |

|---|

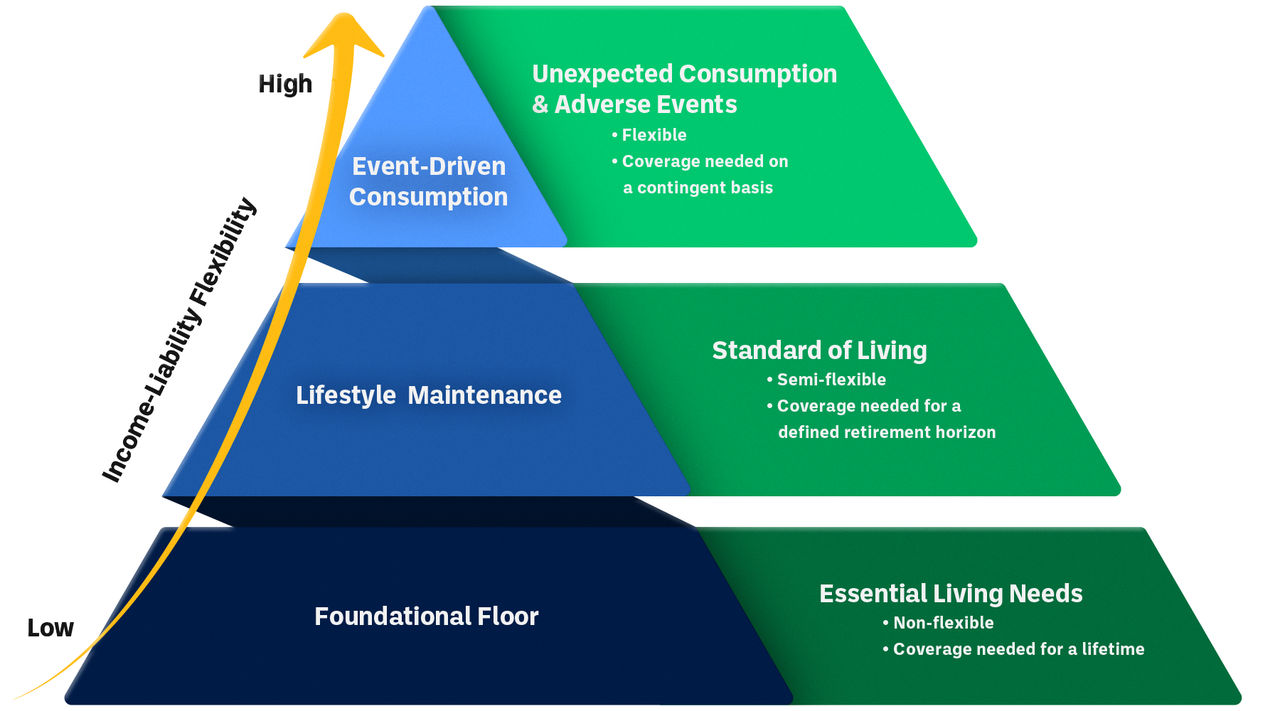

In this article, we outline a framework that organizes participants’ future income liabilities into three distinct layers, each defined by its purpose and risk profile. This layered perspective provides a way to align retirement planning and risk management decisions with the income objectives of each layer.

Layer 1: The Foundational Floor

We define the base layer of retirement income as the foundational floor, representing the income required to meet participants’ essential living needs throughout retirement. These needs include:

- basic housing,

- food,

- health insurance, and

- medical expenses.

By its nature, the foundational floor consists of non-negotiable future income liabilities, characterized by indeterminate individual longevity.

Importantly, these basic needs are also exposed to broad inflation risk, with medical expenses presenting a particularly acute concern. For example, data from the Bureau of Labor Statistics show that between December 2005 and December 2022, the Consumer Price Index for All Urban Consumers (CPI-U) grew at an average annual rate of approximately 2.4%,2 while the CPI for medical care increased at a faster pace of about 3.1% annually.3 Over the long term, medical costs are expected to remain on a structurally higher growth trajectory, with projections indicating a growth rate of about 5% annually from 2036 onward.4 As a result, this layer requires the strictest form of risk governance to ensure income reliability.

| The foundational floor consists of non-negotiable future income liabilities, characterized by indeterminate individual longevity. Importantly, these basic needs are also exposed to broad inflation risk, with medical expenses presenting a particularly acute concern. |

|---|

The primary objective of foundational income is the efficient conversion of capital into dependable income over a lifetime, not the maximization of expected returns. Risk pooling plays a central role in this layer, as it mitigates individual longevity risk by sharing it across a larger population. For example, in the United States, Social Security provides the largest source of guaranteed lifetime income for a broad cross-section of the population, lifting an estimated 17 million individuals aged 65 and older above the poverty line.5 However, the Social Security Trust Fund faces significant long‑term financing challenges: the Old-Age and Survivors Insurance (OASI) Trust Fund reserves are projected to be depleted beginning in 2033, at which point scheduled benefits would be reduced to approximately 77% of promised levels.6

Meanwhile, employer-sponsored pensions and insurer-provided annuities also provide risk pooling benefits and can serve as important complements to Social Security in securing foundational income. Industry research7 suggests that asset allocations incorporating group risk pooling solutions support materially higher sustainable withdrawal rates, exceeding those of fully self-insured strategies by more than 70%.

| The primary objective of foundational income is the efficient conversion of capital into dependable income over a lifetime. |

|---|

Layer 2: Lifestyle Maintenance

The middle layer of retirement income addresses lifestyle maintenance. Beyond meeting basic needs, most participants aim to replace a portion of pre‑retirement income to preserve their standard of living over a period of retirement years, such as 20 or 30 years. Relative to the foundational income floor, these income liabilities are partially flexible, reflecting discretionary lifestyle choices rather than minimum needs.

| Relative to Layer 1, Layer 2's income liabilities are partially flexible, reflecting discretionary lifestyle choices rather than minimum needs. |

|---|

Accordingly, lifestyle maintenance income does not need to be fully realized over all possible longevity outcomes. Instead, retirement income planning is often oriented toward covering income needs over a high-percentile lifetime horizon. Under this framework, individuals who live beyond this planning window may continue to meet essential needs but would likely experience a meaningful reduction in discretionary consumption. Actuarial and academic literature cautions that placing full conviction on a specific assumption, such as average life expectancy, can systematically underestimate longevity risk.8 Consequently, focusing on average estimates overlooks the financial implications associated with the right tail of the longevity distribution (e.g., survival to the 90th percentile of remaining lifetime).

As with the foundational floor, the objective of this layer is not to maximize returns, but rather to convert accumulated retirement assets into a predictable income stream that mitigates the risk of income shortfall and supports lifestyle preservation over an extended lifetime horizon.

| The objective of Layer 2 is not to maximize returns, but rather to convert accumulated retirement assets into a predictable income stream that mitigates the risk of income shortfall and supports lifestyle preservation over an extended lifetime horizon. |

|---|

Layer 3: Event-Driven Consumption

The top layer of retirement income supports event-driven consumption and serves as a buffer against adverse events. Income needs at this layer are contingency-based, encompassing expenditures such as:

- long-term care needs,

- significant health-related circumstances, and

- bequests.

As a result, income associated with this layer can be adjusted in response to market conditions without jeopardizing basic living standards. During periods of economic turmoil and financial stress, income needs associated with this layer may be more easily reduced, deferred, or reprioritized.

| In Layer 3, income needs can be adjusted in response to market conditions without jeopardizing basic living standards. |

|---|

Importantly, while income needs in this layer may be flexible in timing or scale, adverse events can still be financially significant when they occur, highlighting how robust income generation in the foundational and lifestyle maintenance layers improves the ability to withstand and absorb adverse outcomes. Viewed through this lens, the flexibility at the top layer does not eliminate risk but rather shifts its impact, underscoring the importance of stability in the lower layers.

Notably, investment performance during the accumulation stage has relatively limited influence on the foundational and lifestyle maintenance floors, where needs are generally fixed. By contrast, investment performance plays a much more meaningful role at the event-driven consumption layer, where upside investment performance directly expands discretionary spending capacity and legacy potential.

| In contrast to Layer 1 and Layer 2, investment performance plays a much more meaningful role at the event-driven consumption layer (Layer 3), where upside investment performance directly expands discretionary spending capacity and legacy potential. |

|---|

Closing Words

Ultimately, the central challenge in decumulation extends beyond investment selection alone to a deeper issue: the persistent misalignment between how retirement savings portfolios are constructed and how retirement income needs are experienced.

Retirement planning strategies should avoid the continued misapplication of accumulation-stage frameworks to the decumulation stage and instead be designed to address risks across different layers of income needs. For example, research shows that portfolio returns in the first year of retirement explain more than 14% of the long-term retirement outcomes,9 underscoring retirees’ heightened sensitivity to early losses. Unlike during the accumulation stage, retirees are far less able to tolerate short-term volatility once withdrawals have begun. As a result, portfolios constructed under accumulation-oriented frameworks may appear well diversified across asset classes and time horizons, yet still fall short when evaluated through the lens of income reliability.

To address this challenge, and to support lifelong income generation across each layer, the retirement industry needs to deliberately and collectively shift from a return-centric mindset toward one explicitly focused on matching future income liabilities. Consistent with evolving legislation and fiduciary guidance10 aimed at moving defined contribution plans from “savings vehicles” to true “retirement plans,” retirement income solutions should be evaluated based on their ability to meet clearly defined income objectives rather than solely on traditional investment characteristics. Effective risk governance in retirement should therefore emphasize duration matching, withdrawal sustainability, and protection against sequence-of-returns risk, recognizing that different income needs carry different risk profiles and tolerances for variability.

| Retirement income solutions should be evaluated based on their ability to meet clearly defined income objectives. |

|---|

Income strategies capable of supporting retirement outcomes across these layers may include combining short- and long-duration fixed income assets, utilizing income ladders, and incorporating solutions that lock in future income where appropriate. Together, these approaches provide a more resilient foundation for translating accumulated savings into retirement income that is both durable and purpose-aligned.

Insights focused on your priorities

.jpg)

Christine Bass

Head of Defined Contribution Lifetime Income

As Head of Defined Contribution Lifetime Income (DCLI), Christine is responsible for leading the growth of the Defined Contribution Lifetime Income business. Prior to her current appointment, Christine was Head of Specialty Markets where she was responsible for the Institutional Fixed Annuity business. Christine joined Pacific Life in 2022 and has nearly 20 years of experience across life, annuity, and institutional products in U.S. and international markets. Her career has also included roles at Bain Capital, AIG, Milliman, and Prudential Financial. She is a Fellow of the Society of Actuaries and holds an MBA from the University of Chicago, Booth School of Business.

Dr. Qi Sun

Financial Economist, Institutional Division

Qi’s research focuses on longevity insurance, household asset allocation decisions, and financial well-being. Qi holds a bachelor’s degree in finance from Donghua University, a master’s degree in Personal Financial Planning from the University of Missouri, Columbia, and a doctorate in Personal Financial Planning from Texas Tech University. Her 2023 white paper, Decoding Retirement: Key Insights into Participant Preferences for Lifetime Income Options, won multiple awards including a gold and a platinum for best white paper. She is also the recipient of the Journal of Financial Planning’s 2025 Best Research Award and the American Council on Consumer Interests’ 2024 Financial Planning Paper Award. Qi joined Pacific Life in 2021.

1 Merton, Robert C. "The crisis in retirement planning." Harvard Business Review 92, no. 7/8 (2014): 43-50.

2 Data from the U.S. Bureau of Labor Statistics: Consumer Price Index for All Urban Consumers (CPI‑U), December 2005–December 2022 (U.S. city average, All items – CUUR0000SA0).

3 Matsumoto, Brett. "Measuring total-premium inflation for health insurance in the Consumer Price Index," Monthly Labor Review, U.S. Bureau of Labor Statistics, April 2024. https://doi.org/10.21916/mlr.2024.6

4 Getzen Model of Long-Run Medical Cost Trends Update for 2026-2036+, 2025, Society of Actuaries.

5 Social Security Lifts More People Above the Poverty Line Than Any Other Program, Center on Budget and Policy Priorities, 2026.

https://www.cbpp.org/research/social-security/social-security-lifts-more-people-above-the-poverty-line-than-any-other-0

6 The 2025 OASDI Trustees Report.

7 Leveling the Retirement Income Playing Field, AllianceBernstein, 2023.

https://www.alliancebernstein.com/content/dam/alliancebernstein/iim/us/defined-contribution/dc-pdfs/Leveling_the_Retirement_Income_Playing_Field-Executive_Summary.pdf

8 Optimal Consumption and Annuity Equivalent Wealth with Mortality Model Uncertainty, 2022, SOA Research Institute.

https://www.soa.org/globalassets/assets/files/resources/research-report/2022/optimal-annuity-ambiguity.pdf

9 Pfau, Wade D. "The lifetime sequence of returns: A retirement planning conundrum." Available at SSRN 2544637 (2013).

10 The Retirement Income Consortium - Practices for Providing Retirement Income to Participants in Defined Contribution Plans, 2023. https://www.faegredrinker.com/-/media/files/insights/pubs/2023/the-retirement-income-consortium-white-paper.pdf

Christine Bass and Dr. Qi Sun are employees of Pacific Life. The opinions expressed are their own and not necessarily those of the Company.

About Pacific Life

Pacific Life provides a variety of products and services designed to help individuals and businesses in the retail, institutional, workforce benefits, and reinsurance markets achieve financial security. Whether your goal is to protect loved ones or grow your assets for retirement, Pacific Life offers innovative life insurance and annuity solutions, as well as mutual funds, that provide value and financial security for current and future generations. Supporting our policyholders for more than 150 years, Pacific Life is a Fortune 500 company headquartered in Newport Beach, California. For additional company information, including current financial strength and ratings, visit www.PacificLife.com.

Stay up to date on the latest news and opportunities in Defined Contribution Lifetime Income by following Pacific Life’s Institutional Business on LinkedIn.

Pacific Life is a product provider. It is not a fiduciary and therefore does not give advice or make recommendations regarding insurance or investment products. Pacific Life, its affiliates, its distributors, and respective representatives do not provide any employer-sponsored qualified plan administrative services or impartial advice about investments and do not act in a fiduciary capacity for any plan.

This material is provided for informational purposes only and should not be construed as investment, tax, or legal advice. Information is based on current laws, which are subject to change at any time. Clients should consult with their accounting or tax professionals for guidance regarding their specific financial situations.

Pacific Life refers to Pacific Life Insurance Company and its affiliates, including Pacific Life & Annuity Company. Insurance products can be issued in all states, except New York, by Pacific Life Insurance Company or Pacific Life & Annuity Company. In New York, insurance products are only issued by Pacific Life & Annuity Company. Product availability and features may vary by state. Each insurance company is solely responsible for the financial obligations accruing under the products it issues.

The home office for Pacific Life & Annuity Company is located in Phoenix, Arizona. The home office for Pacific Life Insurance Company is located in Omaha, Nebraska.

DCLI0296